Commercial lease deposit rules in the UK: What tenants need to know

Commercial lease deposits are one of the first costs tenants face when taking business premises, but they are often poorly understood. Unlike residential deposits, commercial lease deposits are not usually protected by a government-backed deposit scheme. Instead, the rules are set out in the lease and, most importantly, the Rent Deposit Deed.

This guide explains how commercial lease deposits work in the UK, what tenants should check before signing, and why deposit expectations can vary between Central London, Outer London and regional markets.

What is a commercial lease deposit?

A commercial lease deposit, also known as a rent deposit or security deposit, is an upfront sum paid by the tenant to the landlord before or when the lease is signed. It acts as financial protection for the landlord if the tenant fails to pay rent, breaches the lease, leaves unpaid service charges, or causes damage to the property.

For tenants, it is important to understand that this money is not a fee. It is still the tenant’s money, but it is held temporarily by the landlord as security. The exact rules should be set out in a Rent Deposit Deed, including when the landlord can deduct money, whether interest is payable, and when the deposit must be returned.

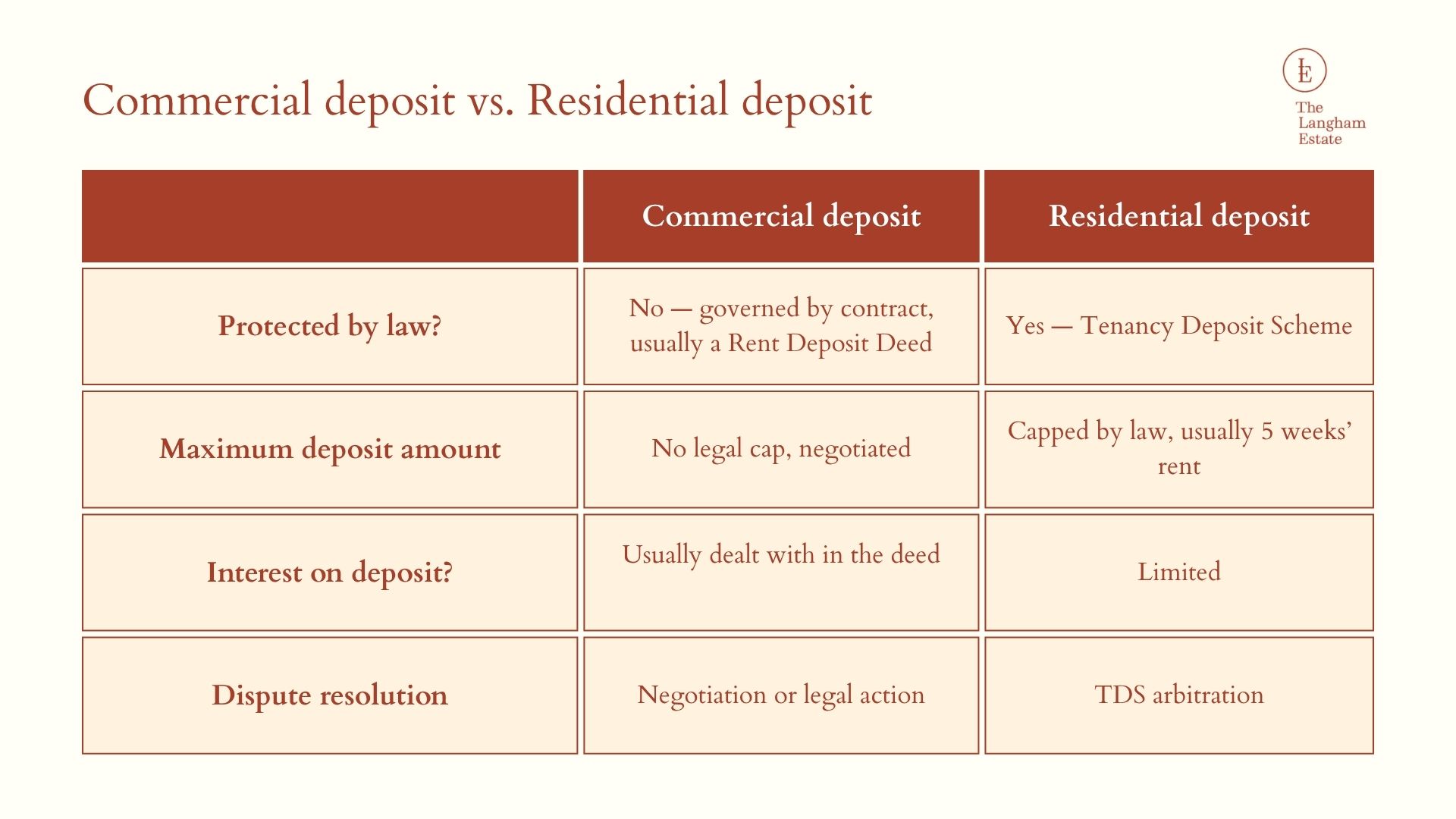

Unlike residential deposits, commercial lease deposits are not usually protected by a government-backed Tenancy Deposit Scheme. That makes the wording of the Rent Deposit Deed especially important.

Important commercial lease deposits that tenants should know

1. Commercial deposits are not protected like residential deposits

Residential tenancy deposits in England are subject to statutory rules, including deposit caps under the Tenant Fees Act. Commercial lease deposits are different. They are usually governed by the lease and the Rent Deposit Deed, not a government-backed deposit protection scheme (Source: Gov.uk).

2. There is usually no fixed legal cap

Unlike some residential letting rules, commercial lease deposits are a matter of negotiation. A landlord may ask for 3, 6, 9 or even 12 months’ rent depending on the tenant’s financial strength, trading history, lease length and perceived risk.

3. Check what the landlord can use the deposit for

Some deeds allow the landlord to draw from the deposit for unpaid rent only. Others may allow deductions for service charge, insurance rent, repairs, dilapidations, legal costs or other lease breaches. Tenants should push for clear limits so the landlord cannot use the deposit too broadly or unfairly.

4. Ask where the money will be held

Ideally, the deposit should be held in a separate, identifiable, interest-bearing account. RICS guidance for commercial property management recommends that property managers establish a separate interest-bearing account for occupiers’ deposits and manage the money and interest according to the legal documents.

5. Watch for VAT and tax treatment

Deposits can have VAT and tax implications depending on how the arrangement is structured and whether the landlord draws on the deposit. Large deposits may also raise SDLT considerations in some circumstances, so tenants should ask their solicitor or tax adviser before completion.

How much deposit can a commercial landlord ask for?

There is usually no fixed legal cap on how much deposit a commercial landlord can ask for. Unlike residential deposits, which are capped by law in many cases, commercial lease deposits are normally agreed through negotiation between the landlord and tenant.

The amount requested may depend on:

- the tenant’s trading history

- company accounts and financial strength

- the length of the lease

- the rent level

- whether the tenant is a new business

- whether there is a guarantor

- the landlord’s view of risk

In practice, a commercial landlord may ask for the equivalent of three to six months’ rent, although some deposits can be higher depending on the tenant’s financial position and the level of risk.

Commercial lease deposits variations, by area

Commercial lease deposit rules do not usually change simply because a property is in Central London, Manchester, Birmingham, Bristol or another UK city. In most cases, the deposit terms are set by the lease and the Rent Deposit Deed, rather than by location-specific deposit rules. A

However, the amount of deposit requested can vary significantly by area. This is because landlords assess risk based on rent levels, tenant demand, property type, and the financial strength of the tenant. Below are the typical deposit benchmarks:

★ For Central London / West End: 6–12 months’ rent

★ For City of London (Bank, Liverpool Street, Moorgate): 6–12 months’ rent

★ For Midtown (Holborn, Bloomsbury, Clerkenwell, Farringdon, King’s Cross): 3–9 months’ rent

★ For Outer London: 3–6 months’ rent

The key takeaway is simple: Where the property is located can affect how much deposit the landlord asks for, but it usually does not change the legal rules. Tenants should always negotiate the amount, release date, interest treatment and deduction rights before signing the lease.

Commercial lease deposit vs. Personal guarantee vs. Parent company guidance

When a landlord is concerned about risk, they may ask the tenant to provide extra security before agreeing to the lease. The three most common options are a commercial lease deposit, a personal guarantee, or a parent company guarantee.

Each option protects the landlord in a different way, but they create different risks for the tenant.

1. Commercial lease deposit

What it means: The tenant pays money upfront, which the landlord holds as security.

Main tenant risk: Ties up business cash that could otherwise be used for fit-out, stock, staffing or operations.

2. Personal guarantee

What it means: An individual, often a company director, personally promises to cover the tenant’s lease obligations if the business defaults.

Main tenant risk: Creates personal financial exposure for the guarantor.

3. Parent company guarantee

What it means: A parent or group company promises to cover the tenant company’s obligations if it fails to do so.

Main tenant risk: Creates financial risk for the wider company group.

Protect your cash before you sign

At The Langham Estate, we believe tenants should enter lease discussions with clarity. Our team manages commercial office space across 14 acres in Fitzrovia, central London, and we are committed to helping prospective occupiers understand the practical details that matter, including deposit expectations, lease terms.

If you are looking for office space in central London and want a transparent conversation before committing, we would be happy to talk.

At The Langham Estate, we believe tenants should enter lease discussions with clarity. Our team manages commercial office space across 14 acres in Fitzrovia, central London, and we are committed to helping prospective occupiers understand the practical details that matter, including deposit expectations, lease terms.

If you are looking for office space in central London and want a transparent conversation before committing, we would be happy to talk.

FAQs

Are commercial lease deposits protected in the UK?

No, not in the same way as residential tenancy deposits. Commercial deposits are usually governed by the lease and rent deposit deed.

How much deposit can a commercial landlord ask for?

There is no fixed statutory amount for most commercial leases. The amount is negotiated and often depends on the tenant’s financial strength and lease risk.

Can a landlord use my deposit for service charge arrears?

Yes, if the rent deposit deed allows it. Tenants should check whether the deposit covers rent only or wider lease liabilities.

Do Central London offices have different deposit rules?

Usually no. The legal rules are not location-specific, but Central London tenants often face higher deposits because rents, service charges and fit-out costs are higher.

Can I negotiate a commercial lease deposit?

Yes. Tenants can negotiate the amount, release triggers, deduction rights, interest treatment and whether alternative security is acceptable.